Central banks are running out of options to manage the fractures in the global financial system. Decades of trade imbalances, fueled by a structural reliance on the U.S. dollar, have pushed major economies into a corner where unilateral economic warfare—via tariffs and capital controls—has replaced cooperation. In policymaking circles, a nostalgic theory is resurfacing: that the world's major economies can simply sit down and orchestrate a modern version of the 1985 Plaza Accord, engineering a coordinated appreciation of Asian currencies to rebalance global trade.

This idea is an absolute fantasy. The structural realities of 2026 make a coordinated currency intervention impossible to achieve and dangerous to attempt. Rather than stabilizing the global monetary system, pushing for a forced rebalancing ignores the massive accumulation of sovereign debt and the weaponization of cross-border capital flows. The global financial system cannot be fixed by central bank alchemy because the underlying imbalances are no longer just macroeconomic anomalies—they are structural features of the modern geopolitical landscape. For a closer look into similar topics, we recommend: this related article.

The Broken Blueprint of the Plaza Accord

To understand why a coordinated intervention cannot work today, one must dismantle the myth of the 1985 Plaza Accord. Four decades ago, the G5 nations successfully engineered a controlled depreciation of the U.S. dollar against the Japanese yen and the German mark. That intervention succeeded because the participating nations shared deeply aligned geopolitical goals and relatively open, unfragmented capital markets.

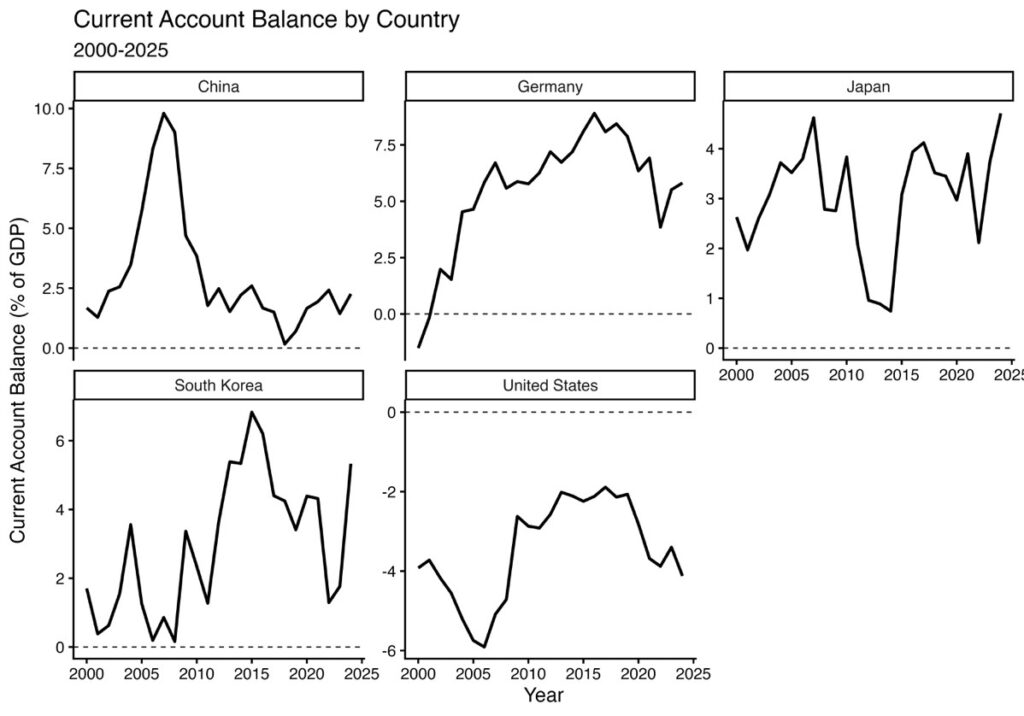

That world is gone. Today, the persistence of massive current-account surpluses in China, Japan, and Germany alongside a permanent U.S. deficit is driven by deep-seated domestic structural dynamics, not merely misaligned exchange rates. Forcing a coordinated currency appreciation across Asia ignores the fundamental domestic constraints faced by these central banks. For additional context on this issue, in-depth reporting can be read on MarketWatch.

Consider Japan. The Japanese yen has faced immense downward pressure, forcing Tokyo to sell off U.S. Treasuries to defend its currency. But the Bank of Japan cannot simply raise interest rates aggressively to support a coordinated appreciation. Japan's public debt sits comfortably above 200 percent of its gross domestic product. Any significant increase in domestic interest rates would instantly crush the country's fragile economic recovery and severely compromise the state’s ability to finance its own debt.

The Sovereignty Trap and Capital Flows

The mechanics of international finance have also fundamentally changed since the twentieth century. The volume of global capital flows is now driven heavily by non-bank financial institutions and private cross-border investors rather than direct trade invoicing alone. When a government aggressively buys or sells foreign currency today, it triggers massive, unpredictable ripples through private portfolios.

Furthermore, direct currency intervention yields vastly different results depending on capital mobility. For a hypothetical country with strict capital controls, every dollar spent purchasing foreign currency might shift its current account by up to 70 cents. But in a highly open economy, that effect drops by more than half, as private capital flows rush in to exploit the arbitrage created by central bank manipulation.

This creates a severe execution gap. Central banks cannot dictate exchange rates when trillions of dollars in private capital can move across borders at the click of a button. Instead of bringing stability, aggressive intervention by one state frequently triggers defensive macroprudential measures, capital controls, or retaliatory tariffs from its trading partners.

The False Promise of Alternative Reserve Assets

As the U.S. dollar remains volatile under the weight of a domestic net international investment position approaching negative 90 percent of GDP, academic commentators frequently argue that the global monetary system will naturally rebalance toward a multipolar reserve framework. They point to the rising prominence of the euro or tech-driven alternative payment mechanisms as proof that the dollar's dominance is ending.

The reality on the trading floor tells a different story. According to recent global central bank surveys, reserve managers have absolutely no intention of meaningfully dumping their dollar assets. Even as central banks aggressively accumulate gold as a geopolitical hedge against financial sanctions, the dollar still commands a massive share of global foreign exchange reserves.

The European Central Bank has openly stated that while the euro can act as a safe-haven during localized risk-off events, it lacks the deep, unified capital markets required to replace the dollar on a global scale. Without a fully integrated fiscal union and a single, massive European sovereign bond market, the euro cannot absorb the trillions of dollars in global liquidity looking for a home. The institutional framework simply does not exist.

The Reality of Fractured Rebalancing

Instead of an orderly, coordinated rebalancing, the global financial system is facing an chaotic fragmentation. Washington continues to deploy unilateral tariffs and industrial policies to shield its domestic market, while surplus nations double down on export-led growth to offset weak domestic consumption.

This zero-sum dynamic means that any attempt at currency diplomacy will inevitably degenerate into mutual recrimination. If a deficit country attempts to force currency appreciation on its trading partners, it will not cure the underlying macroeconomic illness—a chronic shortfall in domestic savings and an insatiable appetite for foreign debt. It will merely accelerate the implementation of retaliatory economic statecraft.

Central banks are not the all-powerful market puppet masters they were in the 1980s. They are guardians of stability operating in a highly politicized, fragmented global arena where structural domestic constraints dictate monetary policy. Expecting a grand international agreement to seamlessly realign global currencies is an evasion of reality. The global monetary system will not be saved by an engineered truce; it will continue to splinter along geopolitical fault lines until nations address the structural imbalances within their own borders.